How to Prepare Bank Statements for 12 Months for Home Loan Application

Introduction: What Do Mortgage Lenders Thing About

You found the house you want. You are ready to apply for a home loan. The lender requests 12 months of bank statements, complicating matters. Most people believe that lenders just want to see your salary coming out of the account every month. That is part of it. But they look at much more than income. Lenders read your bank statements like they read a story. They want to know how you earn, how you spend, do you save and can you actually handle monthly mortgage payments on top of your current lifestyle. A messy or incomplete set is statements can delay your application for weeks. In competitive housing markets, that delay can cost you the property. This guide shows you exactly how to prepare your statements to move your application fast and smooth.

What Months Do Lenders Consider?

Most mortgage lenders request the last 12 months of bank statements. Some may accept 6 months for certain loan products, but 12 months is standard for most home loans in the world. They want a whole year because it has seasonal patterns. Maybe you make more in December because of bonuses. Maybe your expenses increase in September when school fees are due. A whole year contains all of that. If you are self-employed or freelance, some lenders ask for 24 months. They want extra history because your income is not as predictable as a solarium employee. Important point. Lenders want months one after the other. No gaps. If you submit Jan to Dec but skip Aug then they will ask for it. Missing months is cause for suspicion and slows everything down. If you have several bank accounts, expect to submit statements for all of them. Lenders want the full picture and not just the account your salary lands in.

Red Flags Lenders Watch For

Your bank statements can help your application, and they can hurt it too. This is what makes lenders uncomfortable.

Bounced Payments and Failed Debits

If direct debits or bill payments have bounced due to insufficient funds, lenders take notice. It tells them that you ran out of money before the month ended. Even a single or two bounces can raise some questions. A pattern of bounced payments is a serious problem.

Regular Overdraft Use

Dipping into your overdraft every once in a while may not kill your application. But if you live in your overdraft every month, lenders see someone who always spends more than they earn. That is not the profile they want to lend to them.

Large Unexplained Cash Deposits

A large cash deposit that is out of the ordinary of your income pattern is suspicious. The lenders will ask where it comes from. If you cannot explain it using documentation, they may disregard that amount entirely or mark it for further review. This is especially true if the deposit comes right before your loan application. It looks like you are trying to make your finances look healthier than they are.

Gambling Transactions

Regular payment to betting sites or gambling sites is a red flag in many countries. Such behavior is viewed by lenders as a risk factor, as gambling habits can be unpredictable and financially damaging.

High Spending as a Percentage of Income

If you spend 90% of your salary in the first week of the month, lenders wonder how you'll pay your mortgage.

Multiple Buy Now Pay Later Agreements

Several active BNPL plans appear in the form of regular outgoing payments. Too many of these are a signal that you are stretching your finances too thin.

How To Organise and Format your Statements

A well-organized application is processed faster. Here is how to get your statements in order.

Download statements from your bank's website or app. Digital PDF downloads are cleaner and more trustworthy than paper-scanned PDFs. Lenders prefer them.

Label each file clearly. Use a basic naming format such as "BankNameAccountNumberMonthYear." This helps the lender to find what they need without getting confused.

Make sure all pages are included as well. Some statements are long three or four pages. If you only submit the first page, the lender will contact you asking for the rest.

Check for readability of all pages. No blurry scans. No cut-off edges. No pages saved upside down. These small things lead to unnecessary delays.

Put them into chronological order. Oldest Month first, most recent month last. Simple, but it is where many applicants go wrong and it causes confusion.

If you have several accounts, include account statements together. First, calculate the total of all statements from Account A, then calculate the total of all statements from Account B. Do not mix them.

Convert Pdf to Excel For Ease of Review

Here is a tip that most of the applicants miss.

Before you give your statements, read through them yourself. Go through them as a lender would. Look for anything that needs explaining. Check to see that all the months are there. Verify to see if income credits are on a consistent basis.

Doing this in a PDF is painful. You cannot sort transactions, add up totals, or filter by type. Everything is nothing but text on a page.

It is a lot easier to do this review if you convert your statements to Excel. You can sort transactions by amount, eliminate certain payments, and quickly calculate monthly totals of income and spending.

BankStatementMagic.com does this in a matter of seconds. Upload your PDF bank statement and get a nice excel file with all transactions properly organized in columns. BankStatementMagic.com neatly separates dates, descriptions, debits, credits, and balances.

It has more than 1,000 banks around the world. So whether you bank in the US, UK, Australia, India, UAE, or anywhere else it deals with your statement format.

Once you have the Excel file, take 15 minutes to look over your data. Look for anything that looks out of place before the lender finds it. If there is a large cash deposit you forgot about, collect the supporting documents now rather than scrambling.

This small step can save weeks of back and forth during the application process.

Try out free at bankstatementmagic.com.

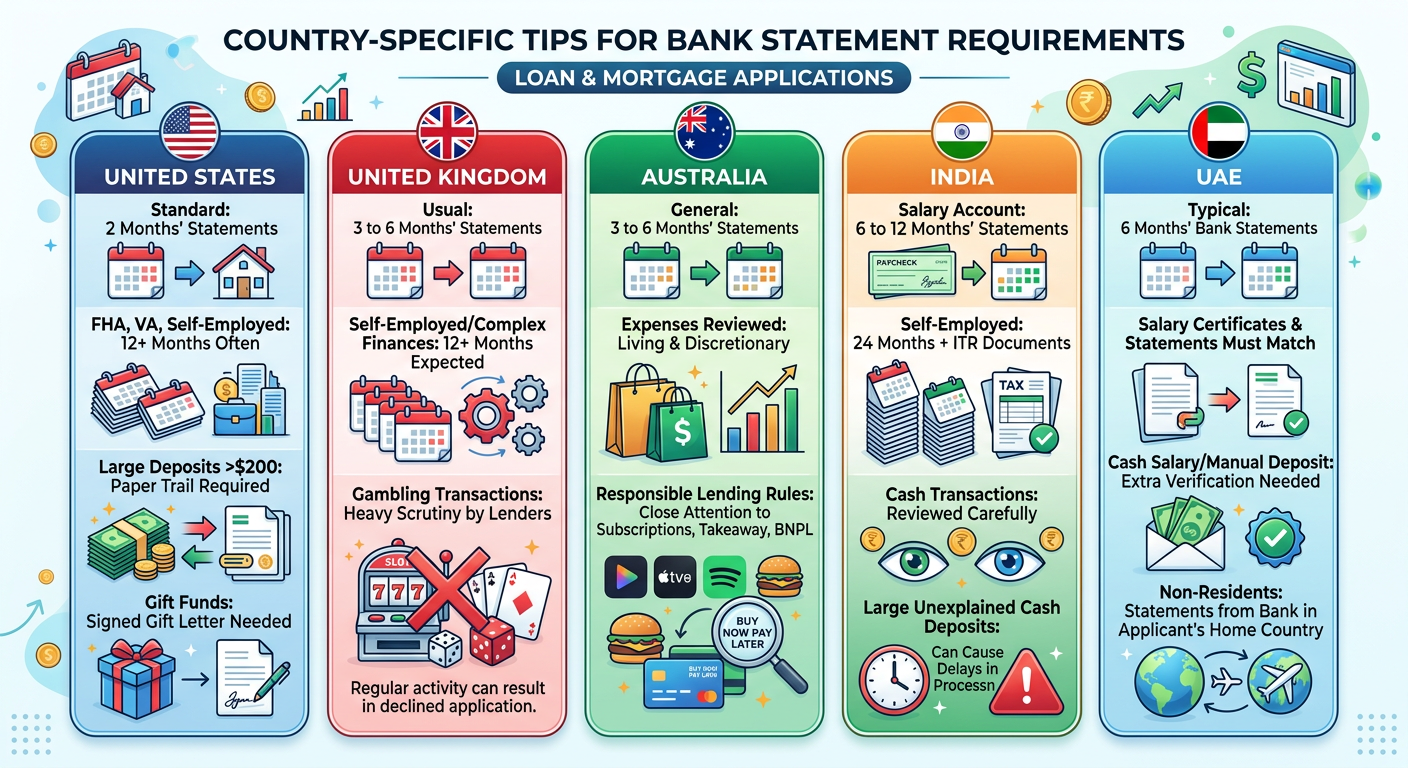

Country-Specific Tips

United States

Most US lenders require 2 months' statements for standard loans. But FHA, VA and self-employment applications often take 12 months or longer. Large deposits greater than $200 require a paper trail. Gift funds for the down payment require a signed gift letter.

United Kingdom

UK lenders usually ask for statements over 3 to 6 months. However, if you are self-employed or have complex finances, expect to have to provide 12 months or more. Gambling transactions are under heavy scrutiny by UK lenders. Regular gambling activity can result in a declined application.

Australia

Australian lenders generally want 3 to 6 months of statements. They take care of living expenses as well as discretionary spending. Since responsible lending rules were tightened, lenders pay close attention to subscription services, takeaway food spending, and BNPL commitments.

India

Home Loan providers in India usually ask for 6 months to 12 months of salary account statements. If you are self employed, then expect to put up 24 months and ITR documents. Cash transactions are reviewed carefully. Large unexplained cash deposits can cause delays in processing to a great extent.

UAE

UAE lenders typically ask for 6 months of bank statements. Salary certificates and statements must be a match. If you receive your salary in cash and as a manual deposit, lenders may require extra verification. To apply for UAE mortgage, non-resident need statements from the bank in the country the applicant lives in.

Conclusion

Preparing bank statements for home loans is not difficult. But doing it carelessly leads to delays, additional questions and sometimes outright rejections.

Give yourself time before you apply. Download all the 12 months of statements and review them yourself. Look for anything that a lender might have questions about and prepare your answers ahead of time.

Convert your PDFs to Excel using BankStatementMagic.com so that you can get a clear look at your own finances before anyone else gets a chance to.

Organize your files. Label them properly. Make sure nothing is missing.

The applicants that are approved the quickest are not always the ones with the highest income. They are the ones who send the clean and complete, well organized documents from the first day.